Payable Through Accounts in Correspondant Banking

Bachir El Nakib

Founder/CEO Compliance Alert LLC

A payable-through account (PTA) is a demand deposit account through which banking agencies located in the United States extend cheque writing privileges to the customers of other institutions, often foreign banks.

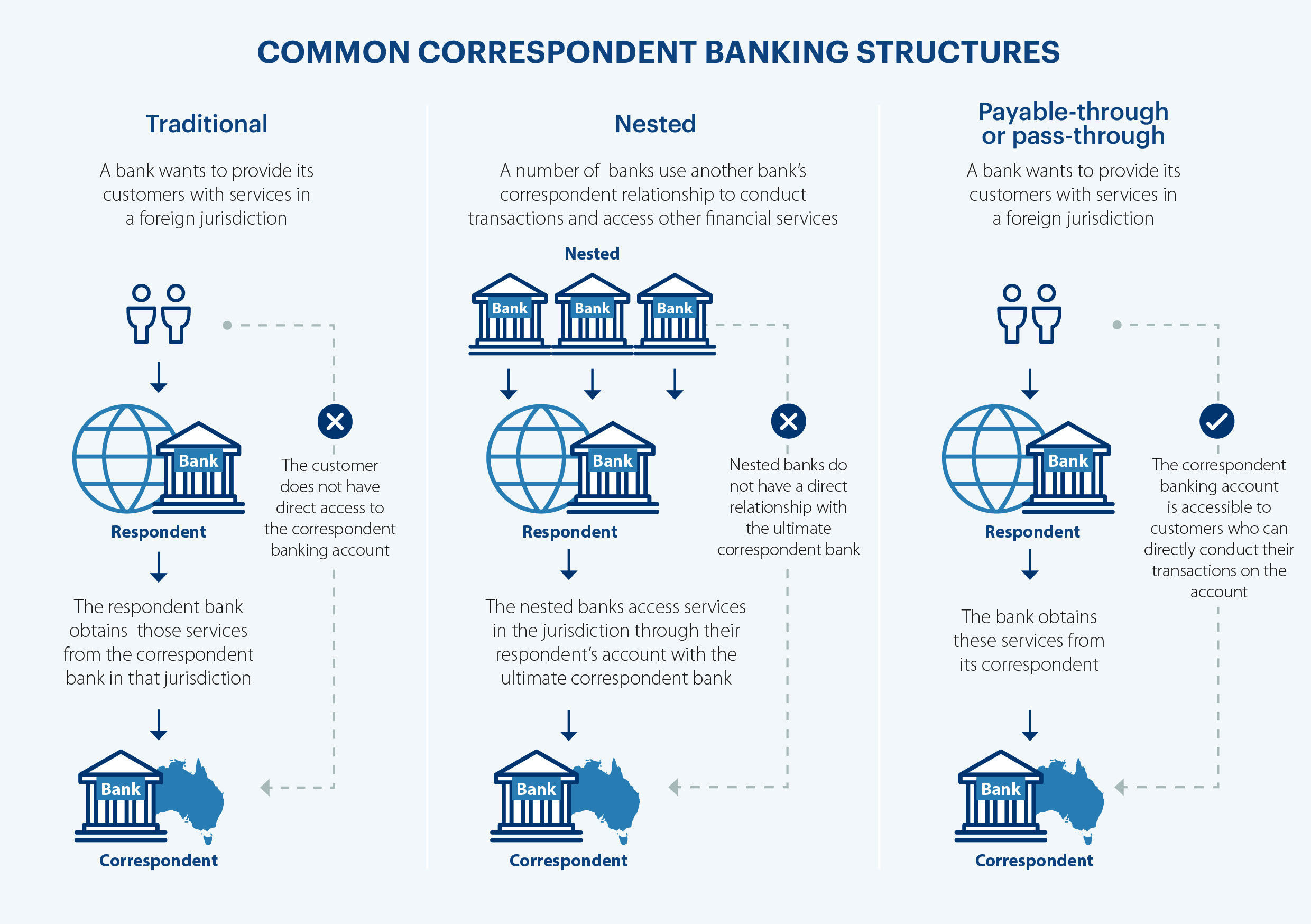

In some correspondent relationships, the respondent bank’s customers are permitted to conduct their own transactions—including sending wire transfers, making and withdrawing deposits, and maintaining checking accounts— through the respondent bank’s correspondent account without first clearing the transactions through the respondent bank.

What does payable-through account means?

The term payable-through account means a correspondent account maintained by a U.S. financial institution for a foreign financial institution by means of which the foreign financial institution permits its customers to engage, either directly or through a subaccount, in banking activities usual in connection with the business in banking

What is the difference between payable-through accounts and Correspondent Banking?

Payable-through accounts, also known as “pass-through” or “pass-by” accounts, are similar to nested correspondent banking but, in this case, the respondent bank allows its customers to directly access the correspondent account to conduct business on their own behalf.

Which accounts are payable?

Accounts payable (AP) is a short-term debt and a liability on a balance sheet where a business owes money to its vendors/suppliers that have provided the business with goods or services on credit.

What are examples of correspondent accounts?

Example. A Dutch oil company is a customer of ING in Amsterdam, and sells a cargo of 500,000 barrels of oil for $40 million to a Swiss trading company who is a customer of Credit Suisse. ING Amsterdam holds its dollars at Bank of America (BofA) and Credit Suisse holds its dollars at The Bank of New York Mellon (BNY).

What are the different types of payables?

Examples of payables include trade payables, non-trade payables, taxes payable, loans payable, and wages payable. The first four of these payables are usually processed through the accounts payable system, while the last type of payable is processed through the payroll system.

What is the difference between correspondent and intermediary?

While correspondent banks normally handle transactions involving multiple currencies, an intermediary bank completes transactions involving only a single currency. They are especially key for domestic banks that may be too small in size to handle these types of transactions.

Payable Through Account (PTA) – In a Nutshell

In some correspondent relationships, the respondent bank’s customers are permitted to conduct their own transactions, directly with the correspondent bank, without clearing these transactions through the respondent bank. These arrangements are called Payable Through Accounts (PTA)

PTA activities are very High Risk Correspondent Services that requires strengthened Due Diligence and Compliance monitoring. Banks that have an AML program will not permit these types of practices.

However, banks still want to make sure that other banks they deal with do not offer it. They can get confirmation of this via a yes/no question on their AML questionnaire.

Those arrangements are called payable-through accounts (PTAs)- CAMS study material.

Payable-Through Accounts (PTAs) and correspondent bank accounts are related concepts in the banking industry, often used in conjunction with each other.

Let us understand some terms related to PTA and Correspondent bank.

1) Payable-Through Accounts (PTAs): PTAs refer to the arrangement where an account holder authorizes a third party, known as a payable-through agent, to initiate payments from their account on their behalf. The account holder, typically a business or organization, maintains the payable-through account with a financial institution.

2)Correspondent Bank Account: A correspondent bank account is a banking relationship between two financial institutions, typically located in different jurisdictions. It allows one bank (the correspondent bank) to provide various services to another bank (the respondent bank), such as facilitating international transactions, clearing payments, and acting as a settlement agent.

3)Relationship: In the context of payable-through accounts, the payable-through agent often operates as a correspondent bank. The correspondent bank maintains its own correspondent bank account with the financial institution where the payable-through account is held. This account serves as the channel through which the payable-through agent initiates payments on behalf of the account holder.

4)Payment Processing: When the payable-through agent receives payment instructions from the account holder, they utilize the funds available in the payable-through account and initiate payments to the designated payees. The correspondent bank account is used to facilitate these payments, ensuring that the funds are transferred efficiently and securely to the payees' accounts.

5)Intermediary Role: The correspondent bank account acts as an intermediary in the payment process. It allows the payable-through agent to access the necessary banking infrastructure and networks to execute payments domestically and internationally. The correspondent bank may also provide additional services, such as foreign exchange conversions or compliance checks, to facilitate the payment process.

6)Reporting and Settlement: The correspondent bank account enables proper reporting and settlement between the financial institution holding the payable-through account, the correspondent bank, and the payable-through agent. It ensures accurate tracking of the payment transactions and facilitates the reconciliation of funds between the different parties involved.

Benefits of Payable-Through Accounts:

1]Enhanced convenience for customers: Customers can make payments to a local account, reducing the need for cross-border transactions and associated fees.

2]Streamlined payment processing: Payments are directly credited to the payable-through account, reducing the administrative burden on the principal.

3] Localization of funds: The principal can access local currency funds, which can be advantageous for operational expenses or investments in the foreign market.

4]Improved cash flow management: The principal can receive payments more efficiently, allowing for better cash flow forecasting and planning.

Payable-Through Accounts (PTAs) can pose certain money laundering threats if adequate safeguards and due diligence measures are not in place.

Some potential money laundering risks associated with PTAs:

1]Layering Transactions:

Money launderers may exploit PTAs to conduct multiple transactions with the intention of obscuring the origin or destination of illicit funds. They may use complex payment structures involving multiple payees and beneficiaries to create layers of transactions, making it difficult to trace the source of funds.

2]Third-Party Abuse:

PTAs involve the delegation of payment initiation to a third-party payable-through agent. If the agent is not properly vetted or monitored, they could be involved in illicit activities, such as using the account to process illicit funds or engage in fraudulent transactions.

3] Lack of Transparency:

PTAs may introduce a lack of transparency, especially when there are multiple layers of intermediaries involved in the payment process. This opacity can make it challenging to identify the true beneficiaries and track the flow of funds, creating opportunities for money laundering.

4]Cross-Border Transactions: PTAs, particularly when combined with correspondent bank accounts, can facilitate cross-border transactions. Criminals may exploit these arrangements to move funds across jurisdictions, taking advantage of varying regulations and weak.

5]Trade-Based Money Laundering:

PTAs can be used in trade-based money laundering schemes. Criminals may manipulate trade invoices, overvalue or undervalue goods, or create fictitious transactions to move funds illicitly. PTAs can be utilized to facilitate these fraudulent trade transactions, making it difficult to identify the underlying money laundering activity.

To mitigate these money laundering risks, financial institutions should implement robust anti-money laundering (AML) and know-your-customer (KYC) measures.

1)Thorough Due Diligence: Conducting comprehensive due diligence on the account holder, payable-through agent, and any involved parties to understand their backgrounds, business activities, and potential risks.

2)Transaction Monitoring: Implementing sophisticated transaction monitoring systems to detect suspicious patterns, such as high-frequency transactions, unusually large amounts, or transactions involving high-risk jurisdictions.

3)Enhanced Customer Due Diligence: Applying enhanced due diligence measures for higher-risk PTAs, such as conducting ongoing monitoring, verifying the legitimacy of payments, and scrutinizing complex payment structures.

4)Regulatory Compliance: Ensuring compliance with applicable AML regulations and guidelines, including reporting suspicious transactions to relevant authorities and maintaining proper records.

5)Training and Awareness: Providing regular training to staff members involved in PTA management to raise awareness about money laundering risks, red flags, and the importance of vigilance in identifying and reporting suspicious activities.

By implementing these measures, financial institutions can enhance their ability to identify and mitigate money laundering threats associated with payable-through accounts, contributing to the overall integrity of the financial system.

Overall, payable-through accounts and correspondent bank accounts work together to enable efficient payment processing and international transactions for businesses. The correspondent bank account serves as a vital link, allowing the payable-through agent to access the necessary banking infrastructure to execute payments on behalf of the account holder.

www.compliancealert.org

Files Related :

There is no files